SA’s telecoms market has been showing signs of saturation for several years. Originally, the sector’s main offering – voice services – provided very high returns on investment. However, the industry now faces what Mike Gresty, a fund manager at Anchor Capital, describes as a transition to data-driven services.

‘The problem for telecommunications companies is that data is much more network intensive,’ says Gresty. However, he points out, ‘this is a competitive industry and customers have become accustomed to falling prices. Telcos thus struggle to pass on the network demands of data services to customers. The result is that returns on capital have steadily declined’. In response to this structural shift, telcos ‘are trying to grow in capital-lite areas such as financial services’, he adds.

PwC Africa technology, media and telecommunications leader Nana Madikane agrees that there has been a big change. ‘There are fundamental shifts in revenue drivers for modern telcos,’ she says. ‘We are in an age of reconfiguration for the industry.’

She suggests there are two thrusts to this. First, there are the ‘growth areas in communication – including fibre, IoT and network sharing for enablement of smart manufacturing/mining, data centre and cloud infrastructure, and fixed wireless home broadband’ and, second, there is ‘adjacent business, including fintech, media and entertainment, and health tech’.

Fintech or mobile money might be an obvious growth path, but it raises the issue of regulation. This is especially the case in countries where the banking sector is strongly entrenched and likely to oppose erosion of what is after all a core part of its business. It is probably why fintech has expanded so much more rapidly in Kenya and other East African markets (Uganda, Rwanda and Tanzania) than it has in SA.

Madikane points out that ‘mobile financial services are thriving in many geographies in Africa. This is almost a tried, tested and proven model to diversify the telco business. Telcos are doing their bit to solve digital inclusion and now moves to solve humanity’s other big problem of financial inclusion’. She adds that there has been an increase in fintech investments over the past year. ‘Fintech investments in East and West Africa show greater returns than Southern Africa. It becomes difficult in placing your bet on the right market to invest in, but it would make logical sense to try and boost the trajectory of growth experienced in the East and West African markets.’

The listed SA telecoms services sector came under pressure in 2023, falling 29% over the course of the year, far exceeding the All-Share Index’s 3% decline. The trend has continued into 2024. Absa Corporate and Investment Bank’s Jono Bradley points out that telecoms counters had fallen a further 16% by the end of February. He suggests that ‘the sector’s key strategic focus [in SA] is to invest in networks to improve quality and uptime, particularly in light of load shedding’.

SA’s two continental giant telecoms operators have started to look more alike in recent years. MTN and Vodacom both have significant assets elsewhere in Africa, in addition to sharing domination of the SA market.

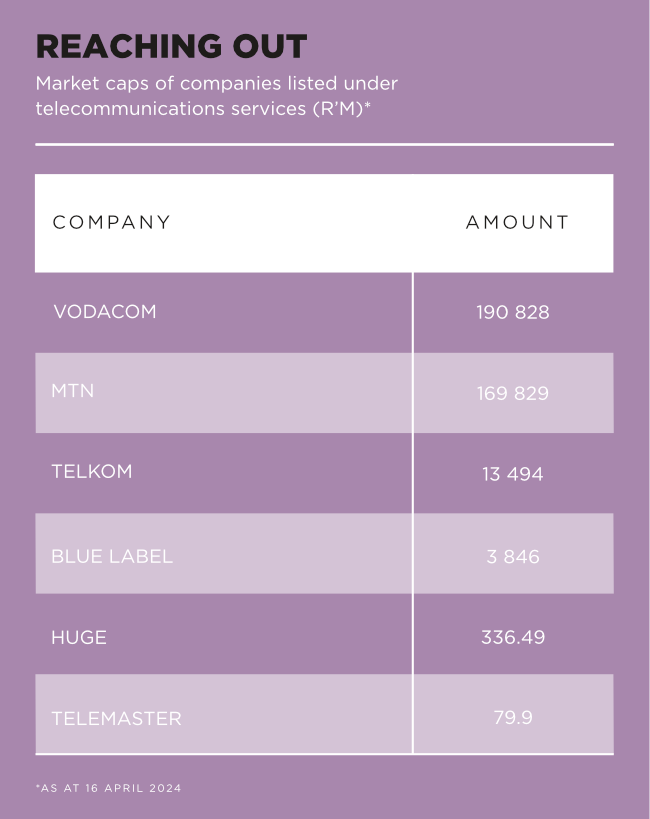

At mid-April, MTN had a market value of R169.8 billion and Vodacom R190.8 billion, far ahead of the third-biggest player, Telkom, with a market value of R13.5 billion. MTN was an early mover into markets outside SA. It is still the biggest telco in Nigeria, the continent’s largest market, which accounts for one-third of the group’s total revenue, as well as 14 other African countries. The company has 76.7 million subscribers in Nigeria. But it has retrenched its Middle Eastern operations, exiting Syria, Afghanistan and Yemen since 2021, retaining only its minority stake in Irantel in the region.

The company is in the process of selling its operations in Guinea, Guinea-Bissau and Liberia, probably to Madagascar-based Axian Telecom. Gresty describes this as ‘a process of de-risking MTN’s portfolio by exiting smaller, under-performing markets, which carry elevated levels of geopolitical risk’. The three West African countries contribute just 1.6% to the telco’s revenue, and it is a smaller player than French giant Orange in all of them.

‘Tough trading conditions persist in the key markets, South Africa, Kenya and Nigeria, in 2024,’ says Bradley. ‘Currency weakness, relative to the US dollar, in all three markets and elsewhere on the continent, has placed growth and margins under pressure, dragging returns lower.’

The key Nigerian market has seen the naira plummet nearly 70% in value after President Bola Tinubu abolished exchange controls in June last year as part of a raft of market reforms. This has weighed on MTN’s share price with the company saying in February that the devaluation had ‘a material effect’ on its results.

MTN’s great rival and contemporary, Vodacom, has chosen to expand strongly in Africa outside of SA in recent years. In November 2022, the company acquired a 55% stake in Vodafone Egypt for R41 billion. Global giant Vodafone – the largest mobile and fixed network in Europe – is Vodacom’s parent company and owns 65.1% of the SA company.

This follows Vodacom’s acquisition of Safaricom, also from Vodafone, in 2017 and its participation in the consortium awarded the second licence in Ethiopia, Africa’s second-largest market by population, in 2021. The Ethiopian operation has yet to deliver a profit.

The move into Egypt is not without geopolitical risks but, according to Vodacom’s February 2024 trading update, it appears to be paying off. The company announced that Egypt had grown service revenue in that country by 29.1% (in local currency) and financial services customers by 55.5% during Q4/23. In the same period, year-on-year revenue growth in SA was only 4%.

However, exchange rate risks have increased in the Egyptian market. In early March, the Egyptian pound lost 60% in value against the US dollar after a central bank decision to allow the currency to float freely. Egypt is experiencing an economic crisis that will feel familiar to South Africans – slowing GDP growth, high interest rates (28%), elevated inflation and a declining currency. How this will affect Vodacom’s investment remains to be seen.

Vodacom CEO Shameel Joosub describes the company’s recent SA performance as ‘satisfactory’ but points out that the comparative period (in 2022) was hit heavily by load shedding. The power outages – combined with ‘vandalism’ including battery theft – have substantially affected the two SA giants, which own most of the country’s base stations (network towers). Vodacom commented last year that it had spent R4.5 billion on resilience to power outages over four-and-a-half years. MTN spent R1.5 billion on its SA Network Resilience programme in 2023 alone. Theft and vandalism cost Vodacom about R120 million to R130 million a year, with the company reporting about 600 incidents every month. Added to consumer weakness, these make SA a tough market at present.

Telcos should focus on differentiating the value they provide to customers and need to make a compelling case, according to Madikane. At the same time, they have to fight off what she describes as ‘increasing competition from MVNO players’.

MVNO (mobile virtual network operators) are companies that do not own a mobile spectrum licence but offer cellular services under its brand name. There are at least 17 such operators in SA, several of them owned by major banking groups (FNB Connect, Standard Bank Mobile and Capitec Connect). Most of them run on Cell C’s network infrastructure.

Cell C is now listed only as a subsidiary of Blue Label Telecoms, which acquired 45% of the company (for R5.5 billion) in 2017. Cell C was originally licensed as SA’s third mobile telephony company. But its licence was awarded only in 2001, six years after MTN and Vodacom, and the company has never been truly competitive. It has faced previous threats of delisting and, on occasion, failed to service debt. In 2019, Blue Label wrote down the value of its investment to zero. In mid-2023 it was valued at just R3.8 billion and had only 7.4% of the SA market by subscribers.

Blue Label Telecoms insists Cell C has a viable future. Blue Label joint CEO Brett Levy points out that it is a well-established brand and argues that ‘it has always been the cheapest for customers […] and can be a nice small third or fourth telco’. From mid-2023 it increased its shareholding to more than 50%, and in early April it received permission from the Competition Commission to take full control of Cell C. The company also shed 4.5 million low-value customers (in 15 months) in a deliberate attempt to ‘rationalise its customer base’.

Both Telkom and Cell C have repeatedly been the subject of rumours of possible take overs or buy-outs. Telkom, which has a fixed-line monopoly, has also struggled in recent years. In 2023 it retrenched 15% of its workforce while in 2020 it suspended dividend payouts for three years. The company has been approached at least three times in the past 18 months by potential buyers (MTN, unlisted SA telco Rain, and a consortium headed by former Telkom CEO Sipho Maseko and backed by Axian Telecom) but has failed to take the bait on any of these occasions.

‘Telkom, with a stretched balance sheet, low revenue growth and negative free cash flows, is facing a challenging outlook,’ says Bradley. Telkom is in the process of selling its masts and towers business, Swiftnet, to Actis and Royal Bafokeng. That may put as much as R10 billion into the company’s coffers. But, as Bradley points out, ‘while the Swiftnet deal may be a positive catalyst for the short term, concerns remain over Telkom’s ability to achieve sustainable cash flows’.

Telkom’s management has announced a strategic vision of the firm as an infrastructure company. But while it says it has R8 billion available in cash and facilities, the industry benchmark is set by MTN and Vodacom, which each burn through about R10 billion a year in infrastructure spending. Selling part of its existing infrastructure holdings – the masts and towers – doesn’t look like a promising start. Nevertheless, Telkom is a respectable-size player in the SA market with 17% subscriber and 14% revenue share.

However, says Gresty, ‘consolidation in the South African market is less likely than one might think’. He argues that the two big players ‘are careful to ensure the survival of the smaller players through network-sharing arrangements because it is not in their interests to see a situation where the regulator attempts to save a failing telco by tilting the competitive playing field’. Bradley agrees. ‘The two leading operators, Vodacom and MTN, need the smaller operators to survive – and thrive – in order to avoid increased and much more stringent regulatory interventions.’

The other companies listed on the JSE’s telecommunications sector are relative minnows – Huge Group (market cap R336.5 million) and TeleMasters Holdings (R80 million). Both are niche operations in the diversified tech investment space. Share prices of both have trended lower over the past three years, reflecting the relative stagnation of SA economy.

Given global, continental and domestic headwinds at the moment, all players can be expected to dig in and take care of their core businesses. Fintech appears to be the face of the future but it is difficult to know which African market to bet on at the moment.